Legal

How State Lawmakers Regulated Marijuana, Hemp, and Kratom in 2025

February 5, 2026 | Kerrie Zabala, Michael Greene

September 22, 2024 | Jason Phillips

-88bbe6-1200px.jpg)

Key Takeaways:

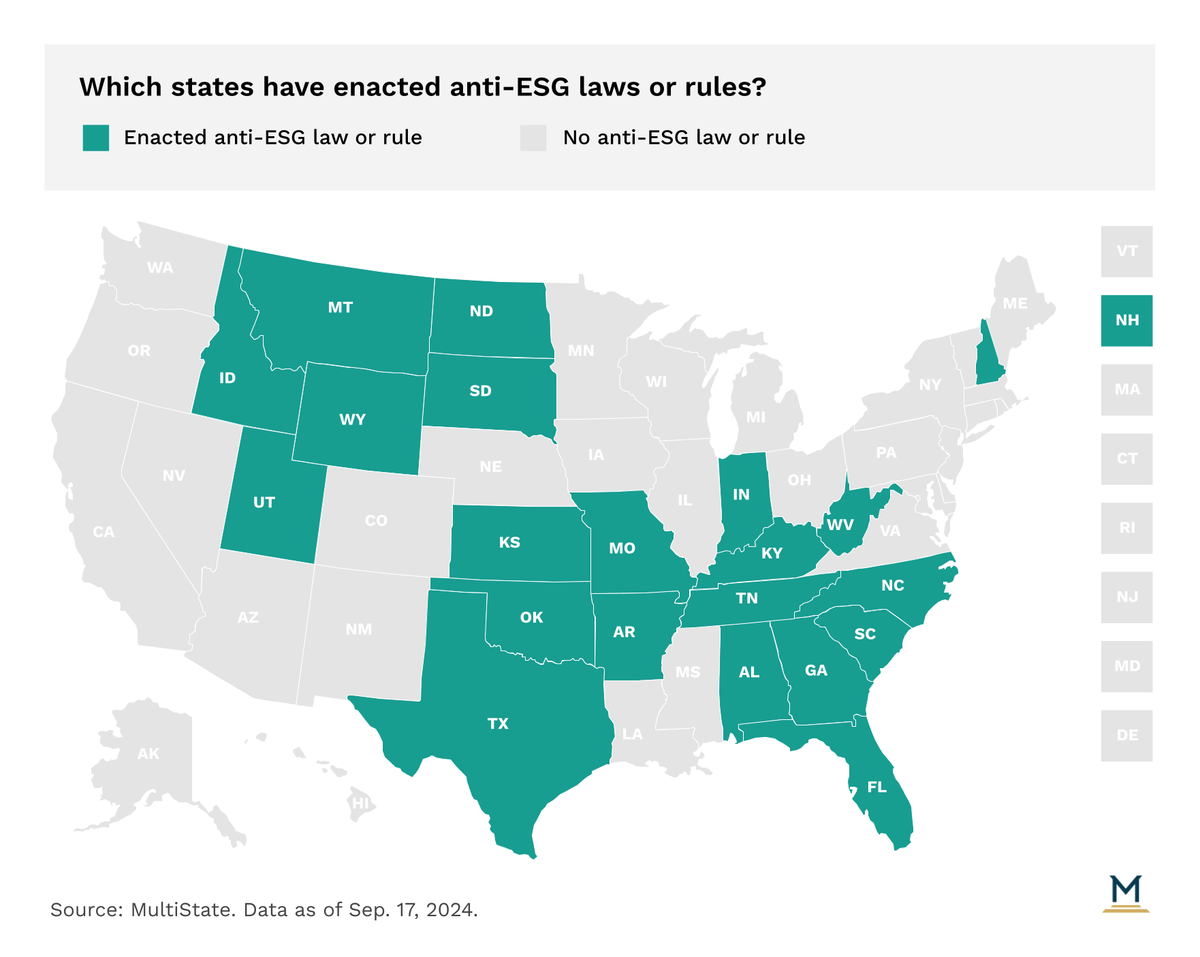

Earlier this year, we highlighted the contrasting situations in New York and Oklahoma on how state pensions are directing investment decisions based on political decisions of fossil fuel companies. And today, the wave of ESG-related (environmental, social, and governance) investment laws that began to pass through state legislatures several years ago have now been in effect long enough for legal challenges to emerge, and anti-ESG laws, in particular, have fared poorly in recent months.

In Missouri, a federal court ruled on August 14 against regulations passed in 2023 that would have required written consent concerning ESG-related investments at several stages of the investment process. Secretary of State Jay Ashcroft initially promulgated the rules last July after the state legislature was unable to reach an agreement on similar legislation. The two rules applied respectively to broker-dealers and investment advisers, and included similar requirements to provide disclosure and obtain written consent when making financial decisions that “incorporate a social objective or other nonfinancial objective into a discretionary investment decision.” A “nonfinancial objective” is defined as “the material fact to consider criteria in the investment or commitment of customer funds for the purpose of seeking to obtain an effect other than the maximization of financial return to the customer.” These steps were required at the initiation of a relationship with a financial adviser, during the sale of a security or commodity, and during the selection process for a third-party investment manager. Thereafter, the rules required annual disclosure from investment professionals and written acknowledgment from a customer no less than every three years, and they included a language template for the customer’s consent. Any failure to follow the rules was classified as a dishonest or unethical business practice.

U.S. District Judge Stephen Bough issued a permanent injunction to stop enforcement of the rules, finding that the rules violated the First and Fourteenth Amendments and were preempted by federal statutes. Firstly, the judge found the regulations are preempted by the National Securities Markets Improvements Act (NSMIA). This federal law works to prevent a complicated dual securities regulation system including both federal and state law, and its record-keeping requirements were found to expressly preempt the Missouri rules. Second, Judge Bough found provisions in ERISA to also preempt the Missouri rules with respect to its mandate to displace state action regarding employee benefit programs. In reaching this ruling, the court rejected the state’s arguments that its record-keeping requirements were innocuous and that it is permitted to regulate securities. Third, the court found a proscribed statement included in the regulations to violate the First Amendment by mandating a disclosure statement that is “not purely factual” and could in fact be misleading. Finally, the rules were found to be unconstitutionally vague, in violation of the Fourteenth Amendment, primarily because they fail to define a “nonfinancial objective” in a satisfactory manner and also provide no written guidelines with additional instruction. The court found this especially troubling in light of the penalties that could be invoked for a failure to abide by the rules.

The Missouri ruling comes just a few months after an Oklahoma County District Court judge granted an injunction against the Oklahoma State Treasurer Todd Russ and his efforts to enforce a law creating a boycott of firms found to discriminate against energy businesses. Judge Sheila Stinson found sufficient evidence of vagueness and violation of exclusive benefit to issue an injunction. The plaintiff had argued that the state constitution requires state pension funds to work “for the exclusive purpose of providing for benefits, refunds, investment management, and administrative expenses of the individual public retirement system” and Judge Stinson agreed, holding that Treasurer Russ’s efforts comprise a political agenda and therefore are unconstitutional. Similarly to the Missouri case, Judge Stinson also found that sections of the law are likely to be found unconstitutionally vague, as key phrases such as “without an ordinary business purpose” were left undefined in the statute. Additionally, the law’s phrasing used multiple definitions of the phrase “governmental entity” without clear distinctions.

These setbacks for anti-ESG laws could spur additional legal challenges. On August 29, 2024, the American Sustainable Business Council filed a lawsuit in Texas to block the state’s 2021 law restricting investment with listed financial firms based on their energy policies. The suit argues that the law violates the First Amendment and infringes on free association. Opponents of the Texas law also claim that it has a harmful effect on the finances of state agencies. Alternatively, proponents of these measures may refine their legislative language to create a formula better able to pass legal muster.

One caveat is that these injunctions are currently being put in place at the district court level, which means we’re likely to see appeals to higher courts before a decision can be made on the merits of the case. Nonetheless, expect to see similar legal challenges to the states that have enacted anti-ESG laws and rules.

This article appeared in our Morning MultiState newsletter on September 17, 2024. For more timely insights like this, be sure to sign up for our Morning MultiState weekly morning tipsheet. We created Morning MultiState with state government affairs professionals in mind — sign up to receive the latest from our experts in your inbox every Tuesday morning. Click here to sign up.

February 5, 2026 | Kerrie Zabala, Michael Greene

February 4, 2026 | Sandy Dornsife

January 26, 2026 | Jason Phillips, Anthony Amatucci